Overview: The US dollar is mixed today. The

dollar-bloc currencies and the Scandis are enjoying a slightly firmer tone, while the

euro and sterling are edging higher in European turnover. The Swiss franc is softer, and the yen

has given back most of yesterday's gains after BOJ Governor Ueda acknowledged

that central bank seeks further confirmation that sustainable price goal is

within reach. We see it as a further signal of an April move on rates rather

than this month. Emerging market currencies are mostly lower but for a few

Asian currencies. The Dollar index is up about 0.25% this week coming into the

North American session. It fell by around 0.35% last week.

Asia Pacific equities rallied today. South Korea and Taiwan were exceptions. Europe's Stoxx is

up around 0.20% in the European morning. It must rise by another 0.25% or end a

five-week rally. US index futures are trading with a softer bias. The Nasdaq is

up 0.6% this week and the S&P 500 is up 0.15% before today's session. European

10-year bond yields are firmer, especially in the periphery, but the benchmarks

are 1-3 bp lower on the week. The 10-year US Treasury yield is off two basis

point to 4.23%. It finished last week near 4.28%. Gold is firmer as its advance

extends into the third consecutive session. The yellow metal is trading above

$2050. It has not closed above there since February 1, when it reached $2065. April WTI is firm above

$79. The high for the year was set on Wednesday near $79.60. Near $79.20, April

WTI is up 3.5% this week.

Asia Pacific

While some

central banks, like the Federal Reserve, say they are data dependent, the Bank

of Japan seems less so. The core CPI, which the BOJ targets

fell to 2.0% last month and looks poised to fall below it this month. The

economy has contracted for the past two quarters, and there is a real risk it

is continuing to shrink this quarter. Yet, BOJ officials appear determined to

finally exit is negative policy rate. It strikes us that officials view the

negative interest rate policy as having reached a point where the costs

outweigh the benefits. It is more of a technocratic decision than a view of the

economic outlook. Comments by BOJ Governor Ueda at the G20 finance ministers

meeting suggested a move in March, speculation of which helped the yen trade

higher yesterday, was unlikely. The yen returned toward its recent lows after

Ueda's comments were published. We continue to see April as a likely timeframe.

The results of the spring wage round will be known (March 15), and the

government's electricity and gas subsidies are scheduled to end, which will

lift headline inflation.

China's

February PMI were little changed from January. The

manufacturing PMI stands at 49.1, down from 49.2 in January. The low reading

last year was in May at 48.8. The non-manufacturing PMI rose to 51.4 from 50.7.

It is the third month of improvement. It was last above there in September 2023

(51.7). The composite PMI stands was unchanged at 50.9. It was at 56.4 last February.

The Caixin manufacturing PMI has fared better than the "official"

one. It edged up to 50.9 from 50.8. Next week's meeting of the National

People's Congress and the Chinese People's Political and Consultative

Conference are important events. The official growth target (which seems like

an input rather than an output) is expected to be announced (5%?). Personnel

changes are expected and although some platitudes about the private sector may

be announced, the Communist Party continues to broaden its presence and Xi know

no rival.

The yen had

an outsized reaction to the BOJ board members comments about inflation and

expectations reaching a critical point. Ueda's comments unwound most of the

yen's gains, but the swaps market is a different story. Yesterday, the swaps

market showed none of the drama of the spot fx market. The overnight index swap

for the meeting later this month rose by half of a basis point to 2.6 bps. It

rose by another half of a basis point today to 3.1 bp. The peak in January and

February was 35 bp. The OIS for April rose 3/10 of a basis point to 8.4 bp

yesterday, but slipped slightly to 7.8 bp today, where is also settled last

week. Japan's two-year yield is the highest since 2011, but it only rose by

about 8/10 of a basis point to almost 18 bp yesterday and another basis point

today to finish the week at 19 bp. That is a3.5 bp increase on the week. The

dollar found support in the North American morning near JPY149.20, the lowest

since February 12, the day before the US CPI was reported. It recovered to

closed slightly above the 20-day moving average (JPY149.20). The dollar reached

almost JPY150.70 in the European morning. A close below JPY150.50 is needed to

snap the dollar's eight-week advance against the yen. That matches the longest

rally since November-December 2013. With rate expectations converging with the

Fed's Q4 23 views and our expectation of generally softer economic data, the 50

bp rise in the US 10-year yield, which the exchange rate appears to track, may

have run its course. This may reinforce the cap in the JPY151-JPY152

area.

The Australian dollar stabilized yesterday after Wednesday's

drubbing, but it still looks vulnerable. The five- and 20-day moving

averages have turned down and the Aussie failed to close aback above $0.6500,

though it is straddling the area today, having reached almost $0.6515 in late

Asia Pacific turnover. The daily momentum indicators are turning lower. A

three-week rally is ending, and the Aussie has fallen more this week (~0.90%)

than it had risen in the previous three weeks. The Chinese yuan

continues to appear to track the yen. The yen's recovery yesterday saw the

yuan trade at five-day highs, and its reversal today, has seen the greenback

return to the CNY7.20 area that marks the cap. The PBOC set the dollar

reference rate at CNY7.1059 (CNY7.1036 yesterday). The average of Bloomberg's

survey was CNY7.1978 (CNY7.1935). The dollar settled last week near CNY7.1965.

It has risen in all but one week here in 2024.

Europe

The eurozone's

preliminary February CPI estimate stands at 2.6%, down from 2.8% in

January. The core rate is at 3.1%, down from 3.3% in January and is the

lowest in two years. The 0.6% monthly rise in the headline rate brings the

three-month annualized rate to about 1.6% and the six-month annualized rate to

almost 0.5% (no typo). The European Central Bank meets next week. It is still

too early to look for a rate cut, but the economic forecasts will be updated.

This year's CPI forecast of 2.7% seems high as does the growth projection

(0.8%).

The week ahead

continues to see a light calendar of market-moving high frequency British

economic data. The highlight next week is the Spring Budget, which is widely

expected to include some tax cuts as the Tories prepare for an election, seen

later this year. There has been speculation of a cut in the tax for the

National Health Services and a small cut in basic income tax rate. However,

personal allowances have been frozen since 2021, an un-freezing them would have

greater impact than a small tax cut. Some reports suggest the fuel tax duty

that is scheduled to be increased next month could be canceled and paid for by

extending the windfall tax on oil and gas companies (due to expire in March

2028). Separately, the final manufacturing PMI readings for Germany and France

were slightly between the than initial estimates, but at 42.5 and 47.1

respectively, there is little encouraging news here. Spain is more promising

with a 51.5 read, its best since June 2022. Italy's manufacturing PMI stands at

48.7 up from 48.5 in January. Note that the UK's manufacturing PMI final

reading rose to 47.5 (from 47.1 preliminary reading and 47.0 in January).

The euro made

a marginal new six-day low but continues to hold above important technical

support near $1.0790. The market does not appear done trying. The bounce

after the low early in the North American afternoon yesterday stalled near

$1.0810 and today's bounce fizzled slightly above $1.0820. It is difficult to

imagine a euro-bullish message from the ECB next week. Although intermittent

support may be seen around $1.0770, on a breakdown, there is little to stand in

the way of the test on the February low slightly below $1.07. In recent

days, sterling probed the middle of the old trading range near $1.27 but failed

to close above it. Yesterday, it settled on its lows and below the

20-day moving average. It reached about $1.2640 today in late Asia Pacific

turnover before being sold to session lows in early European activity a little

below $1.2620. The trendline connecting the two February lows comes in near

$1.2565 today, slightly below the 200-day moving average (~$1.2575).

America

Economists do

a good job interpolating the PCE deflators after the CPI and PPI are in

hand. And indeed, they matched the median forecast in Bloomberg's

survey. The surprise was the 1% jump in personal income. The median forecast

was for a 0.4% gain and instead it came in at 1.0%. We often think of income

being driven by wages and salaries. In January, dividends seemed to account for

about a third of the increase in income, and the increase in Social Security

payments (cost-of-living adjustment) was worth about 20% of the increase.

There are two

type of US data that will be reported today. The first are

surveys. They include in the final manufacturing PMI, the manufacturing ISM,

the KC Fed's Services Activity, and the final February University of Michigan

consumer survey. Second are the real sector reports. There two: January

construction spending and auto sales. Construction spending rose by an average

of 1.1% in 2023. As part of the general slowing of US growth, construction

spending will also likely moderate. The median forecast in Bloomberg's survey

is for a 0.2% gain after a 2.2% rise in January 2023. If the median forecast is

accurate, it would be the weakest January reading since 2017 (when construction

spending fell by 1.2%). Note that the data is sufficiently important as to

prompt the Atlanta Fed to update its GDP tracker after doing so yesterday (3.0%

vs. 3.2% previously for Q1 24). The Atlanta Fed will update its tracker before

the vehicle sales are known. Vehicle sales fell 5.2% in January to a 15 mln

unit seasonally adjusted annual pace. The median forecast in Bloomberg's survey

calls for about a 2.5% increase to 15.4 mln vehicles. That would mean a 15.2

mln average in the first two months of the year compared with 15.3 mln for the

Jan-Feb 2023 period. Next week, the market's attention turns back to the US

labor market. On top are JOLTS, ADP, and most importantly, the nonfarm payroll

report. The median forecast in Bloomberg's survey is for a 180k increase in

nonfarm payrolls after 353k was estimated in January.

Canada also

reports its February jobs data at the end of next week. But, ahead of

it, on Wednesday, March 6, the Bank of Canada meets. It is too early for the

Bank of Canada to move. The swaps market has about an 80% chance of a cut in

June, virtually unchanged on the week. The market is pricing in three rate cuts

this year and a 40% chance of a fourth cut. A week ago, only three cuts were

discounted. Mexico sees its manufacturing PMI and the IMEF surveys today.

Mexico also reports January worker remittances. There is a strong seasonal

pattern for remittances to decline from December (past 19 consecutive Januarys

without fail). Next week's highlight for Mexico is the February CPI on March 7.

A continued moderation is expected, and this may fan speculation of a rate cut

at the March 21 Banxico meeting. Brazil reports Q4 23 GDP today and February

vehicle sales. The economy eked out a 0.1% gain in Q3 23 and may be fortunate

to repeat that in Q4.

The US dollar

traded inside Wednesday's range yesterday and is inside yesterday's range so

far today. Inside days are often seen as reversals. But it does

not look like the greenback bulls have been satiated. The greenback held the

five-day moving average, slightly below CAD1.3540 and settlement was little

changed near CAD1.3580. The Canadian dollar has fallen every week this year so

far but one (week ending Feb 9 when it rose by 0.02%). It was off 1% in

February and almost 1.5% in January. The immediate cap can be found in the

CAD1.3600-25 area. The Mexican peso was the strongest currency in the

world in February, rising almost 1% against the US dollar. For the

past five sessions, the dollar has traded in the range set on February 22

(~MXN17.0120-MXN17.1570). It may stay in that range today. The downtrend line

we are monitoring comes in near MXN17.08 today and around MXN17.0250 at the end

of next week. The dollar held barely below BRL5.0 yesterday and has not closed

above there since the end of last October. The lower end of the recent range is

BRL4.91-BRL4.92. The real slipped by about 0.35% in February after losing

almost 2% in January.

Overview: The dollar is mixed as the market awaits

the US personal consumption expenditure deflator, which is the measure of

inflation the Fed targets. While there is headline risk, we argue that the

signal has already been generated by the CPI and PPI releases. The yen is the

strongest of the G10 currencies, up nearly 0.5%. The market shrugged off weak

data that spurs speculation of a third quarterly contraction and focused on the

comments from a BOJ board member that were consistent with the exit from

negative interest rates in the coming months. Meanwhile, the Australian and New

Zealand dollars remain fragile after yesterday's drubbing. Most emerging market

currencies are firmer today, led by the Malaysian ringgit, where officials are

threatening to intervene.

Asia Pacific equities were

mixed, including in Japan where the Topix edged higher, but the Nikkei slipped.

Mainland Chinese stocks rose with the CSI 300 up almost 2%. However, Chinese

companies that trade in Hong Kong fell by about 0.2%. South Korea and Taiwan

went in opposite directions as did Australia and New Zealand. Europe's Stoxx

600 is slightly firmer after falling by 0.35% yesterday. US index futures are

trading softer. Bonds are selling off. European benchmark 10-year yields are

4-6 bp higher. The 10-year US Treasury yield is up four basis points to nearly

4.31%. Gold is a little softer but within yesterday's range (~$2024-$2038). April

WTI is flattish near $78.50.

Asia Pacific

Japan's economy continues to

struggle. After

dropping 2.6% in January, the most since the early days of the pandemic,

Japanese retail sales edged up by 0.8% in January. Although economists,

including the IMF continue to bang the drum about weak Chinese consumption,

though it has doubled on a per capita basis over the past decade and is

growing, Japan has been given a free ride. In GDP terms, its consumption has

fallen for three consecutive quarters through Q4 23. It might be stabilizing

this quarter, but next week's labor earnings data will show real wages continue

to lag inflation as has been the case since 2019 on an annual basis.

Separately, Japan reported a dramatic 7.5% plunge in January industrial output.

It grew by a little more than 1.2% all last year. Recall that a 7.5-magnitude

earthquake struck northern Japan on January 1 and disrupted economic activity.

There was also a safety scandal at a subsidiary of Toyota that also caused a

temporary halt of production. A recovery appears underway this month. Factory

output is expected to rise 4.8% this month and 2% in March. Separately, Japan

reported a 7.5% drop in January's annualized housing starts, which last rose in

May 2023.

However, the impact of the

data was overwhelmed by the comments from Takata, from the BOJ board. He said that despite the economic

uncertainties, the "price target is finally coming into sight."

Takata said that the deflationary psychology was pivoting. Japan's 10-year

yield edged up and the yen jumped. Indeed, the dollar was sold below the 20-day

moving average (~JPY149.80) for the first time since the US employment data on

February 2. The poor economic data and the softness of inflation may have seen

some participants waver, but it still seemed to us that an exit from negative

rates in April remained the most likely scenario. And that still is the base

case.

China's PMI will be reported

tomorrow. It will

likely show the manufacturing sector continues to be challenged (below the 50

boom/bust level), as it has last March with one exception (September 2023). The

non-manufacturing, which some suggest is a better reflection of domestic

demand, held above 50 all last year. It finished 2023 at 50.4 and may have

ticked up in February amid anecdotal reports of strong holiday activity. If it

does rise, it would be for the third consecutive month. The composite PMI rose

to a four-month high of 50.9. The Caixin manufacturing PMI will also be

reported. It has fared better than the other one (from China Federation of

Logistics and Purchasing.

The dollar held barely below

the high set earlier this month near JPY150.90 yesterday and the BOJ comments

today saw it fall to almost JPY149.60, the low since the US CPI on February 13.

It recorded range that

day of approximately JPY149.25-JPY150.90 and has been in that range ever since.

The dollar settled last week near JPY150.50. It was the eighth consecutive

weekly gain, and that streak is threatened now. The net speculative

(non-commercial) short yen position in the futures market is the largest since

last November. The Australian dollar stabilized after falling almost 1%

yesterday but could not properly recover. After falling to about

$0.6490, the Aussie could barely trade above $0.6505 in North America. Today,

it rose slightly above $0.6520 in the Asia Pacific session but is slipping back

below $0.6500 in the European morning. The $0.6475 area stands in the way of a

retest on the year's low near $0.6440 when the US CPI was reported on February

13. The recovery of the yen helped Chinese officials defend the CNY7.20

level. The PBOC set the dollar's reference rate at CNY7.1036

(CNY7.1075 yesterday). This allows the dollar to trade in a range of roughly

CNY6.9615 to CNY7.2457. The average projection in Bloomberg's survey was

CNY7.1935 (CNY7.2004 yesterday).

Europe

The preliminary estimate of

the eurozone's February CPI will be reported tomorrow. The median forecast in Bloomberg's survey

is for a 0.6% increase after a 0.4% decline in January. Recall that in February

2023, the CPI rose by 0.8%. That means that the year-over-year rate can slip to

2.5%-2.6% from 2.8% in January. The eurozone's CPI jumped by 0.9% and 0.6% in March

and April 2023, and will be replaced with more moderate numbers this year. This

means that when the ECB meets on April 10, CPI will be close to 2% and poised

to slip below the target. German states reported softer year-over-year CPI

today and the aggregate harmonized measure, due shortly, is expected to fall to

2.7% from 3.1%. France's harmonized measure fell to 3.1% from 3.4%. Spain's

eased to 2.9% from 3.5%. The swaps market has nearly a 90% chance of a rate cut

in June. Three cuts and about 40% chance of a fourth cut are reflected in the

swaps market.

The euro briefly slipped

below $1.08 for the first time in a week yesterday just at start of the

European session. It

recovered back to the session high, slightly below $1.0850 before it

consolidated in dull dealings in the North American afternoon. The bulls may

see a hammer candlestick, and the 20-day moving average held (~$1.0790), which

is also the halfway point of the bounce from the February 14 low slightly below

$1.07. The euro managed to settle above the 200-day moving average (~$1.0830).

It had advanced for eight of the ten sessions through Monday and brings a

two-day decline into today. It has traded with a firmer bias today and edged up

to almost $1.0855. The week's high was set on Tuesday near $1.0865 and

recapturing this would help the technical tone. Sterling's price action

was also not impressive, and it did briefly trade below its 20-day moving

average (~$1.2630). It recovered about half-of-a-cent before sellers

reemerged and knocked it back to $1.2645. Sterling had not fallen since

February 19. It is in less than a quarter-cent range today below $1.2675. With

little market reaction, the UK named the OECD's Chief Economic Economist

Lombardelli to succeed Broadbent as deputy governor of the Bank of England,

whose term ends July 1. Today's byelection in the Rochdale is very

idiosyncratic and will be difficult to generalize. Separately, there are

reports of discussions between the US and the UK about the potential security

risks of holding national elections around the same time.

America

Although US Q4 23 GDP was

revised lower (3.2% vs. 3.3%) consumption was revised higher (3.0% vs. 2.8%). The deflators were also tweaked higher.

However, the January data reported yesterday disappointed. The advanced

merchandise trade deficit widened to a six-month high of $90.2 bln, and retail

inventories rose by 0.5% after a 0.6% increase in December. Wholesale

inventories slipped by 0.1%. This is consistent with the recent pattern whereby

wholesalers are reducing inventory while retails ae see their inventories rise.

Last year, wholesale inventories fell by an average of 0.2% Retail inventories

rose by an average of 0.4% a month last year.

Today's focus is on the

personal income, consumption, and deflators. If US economic activity is going to

moderate, the consumer is key. Personal consumption expenditures rose by an

average of 0.5% a month last year. The weakness in retail sales hinted at a

pullback in the American consumer, who buys more services than goods. The

median forecast in Bloomberg's survey is for a 0.2% increase. Personal income

rose by an average of 0.4% a month in both 2022 and 2023, which is also the

average of the two years before Covid. Many participants are more interested in

the deflator, but with CPI and PPI in hand, economists have a fairly good sense

of the PCE deflators A 0.3% increase in the headline deflator in January

will bring the year-over-year rate to 2.3%-2.4% (from 2.6% in December 2023),

which would be the slowest pace since February 2021. The core deflator is seen

rising by 0.4%, which would allow the year-over-year rate to slip to 2.8% from

2.9%. When the January CPI was reported on February 13, the implied yield of

the December 2024 Fed funds futures contract soared by 23 bp and the Dollar

Index jumped by about 0.75%. Because of the limited new information in deflator

today, the market response should also be constrained.

Canada reports December and

Q4 23 GDP today. Unlike

the UK and Japan, which reported back-to-back quarterly contractions, the

Canadian economy is likely to have returned to growth after a 1.1% annualized

contraction in Q3 23. A 0.8%-0.9% expansion seems likely. The monthly GDP

estimates contracted in June and July and were flat in August through October,

before the economy grew by 0.2% in November. It is expected to have grown by

another 0.2% in December. Ahead of the data, which we think is in line with the

central bank's expectations, the swaps market is pricing in about a 70% chance

of a cut in June. It has three cuts fully discounted this year and almost a 25%

of a fourth cut. At the end of last week, there was around a 76% chance of June

cut and only three quarter-point cuts were envisioned for this year.

The US dollar reached a new

high for the year yesterday, breaching the CAD1.3600 level in early North

American turnover. It

pulled back and found support near CAD1.3560. It finished near CAD1.3575, its

highest settlement since mid-December. We had seen risk extending to

CAD1.3600-CAD1.3625. A move above there could spur another big figure advance

(CAD1.3700-CAD1.3730). A break below CAD1.3525, and ideally, CAD1.3500 would

neutralize yesterday's constructive price action. So far today, the greenback

is quiet but firmly trading between CAD1.3570 and CAD1.3590. The

Mexican peso is the strongest emerging market currency this month, gaining

about 0.85% against the dollar. That puts it in third place for the

year behind the Indian rupee, the only emerging market currency to have edged

higher against the greenback (~0.35%) and Hong Kong dollar (~-0.2%). The peso

has off by about 0.60% this year. Still, the dollar continues to fray the

downtrend line that we have been tracking off the January 23 and February 5 highs

but has not settled above it. We have it coming in near MXN17.09 today.

![]()

![]()

![]()

The Japanese yen has edged higher on Wednesday. In the European session, USD/JPY is trading at 151.17, down 0.26%.

Yen falls to 34-year low, will Tokyo intervene?

The Bank of Japan raised interest rates last week for the first time since 2007. The move marked a sea-change in monetary policy. However, the tightening has not translated into gains for the Japanese yen, which remains under pressure. Earlier today, the yen fell as low as 151.97, its lowest level since 1990.

Will the yen's slide trigger a currency intervention from Japan's Ministry of Finance? The MOF intervened last October when the yen dropped to 151.94, which means we are clearly within "intervention territory". The MOF's response to the current decline, however, has been limited to verbal intervention.

On Monday, as the top currency diplomat, Masato Kanda, sent a warning to speculators that he was concerned by the yen's slide, saying it did not reflect fundamentals. Earlier today, Japan's finance minister, Shunichi Suzuki, warned that excessive movement by the yen would be answered with "decisive steps".

Japanese officials have limited their response to the yen's woes with jawboning but the risk of intervention is very real and will increase if the yen continues to lose ground. Still, it should be noted that last year's interventions didn't really get the job done, as yen gains were short-lived.

The lack of certainty as to whether Tokyo will intervene to prop up the yen could result in volatility for USD/JPY and investors will be listening carefully to every comment coming out of the BoJ or the MOF.

USD/JPY Technical

USD/JPY remains range-bound on the weekly chart:

![]()

![]()

![]()

The Japanese yen continues to have a quiet week. In the North American session, USD/JPY is trading at 151.36, down 0.03%.

BoJ core inflation eases to 2.3%

Bank of Japan core inflation fell to 2.3% in February, down from 2.6% in January and shy of the market estimate of 2.5%. The release further complicates the inflation picture in Japan, as we continue to see inflation indicators heading in all directions. The BoJ core inflation index eased in February ,while the services producer price index climbed 2.1%, unchanged from January.

The BoJ made a massive pivot last week as it raised interest rates for the first time in 17 years. The central bank is counting on rising service inflation replacing cost-push inflation as the main driver of inflation, which it expects will make inflation sustainable around the 2% target.

The shift in monetary policy has not translated into a win for the yen, which is above the 151 line. There is the threat of currency intervention, as Tokyo intervened last September and October when USD/JPY rose above 152. Japanese officials are trying to jawbone the yen higher before resorting to intervention, with Japan's top currency diplomat sending a warning on Monday to speculators from trying to sell of the yen, saying the currency's recent slide did not reflect fundamentals.

In the US, it was a mixed day. Durable goods recovered in February with a gain of 1.4% m/m in February. This followed a 6.9% slide in January and beat the market estimate of 1.1%. The Conference Board consumer confidence index was almost unchanged at 104.7 in February, compared to 104.8 a month earlier. This was shy of the market estimate of 107.

USD/JPY Technical

![]()

![]()

![]()

The Australian dollar has extended its gains on Tuesday. In the European session, AUD/USD is trading at 0.6557, up 0.26%. On today's data calendar, the US will release two tier-1 events. Durable goods orders are expected to rebound with a 1.1% gain in February, after a 6.1% slide in January. The Consumer Board consumer confidence index is expected to tick up to 107 in February, up from 106.7 in January.

Australian CPI expected to rise slightly in February

Australia's inflation rate is expected to creep up in the February report, which will be released on Wednesday. The market estimate stands at 3.4% y/y for February, compared to 3.4% in January.

That could set back expectations for a rate cut from the Reserve Bank of Australia, which has kept rates unchanged at 4.35% for four straight times. The markets are of the view that the RBA's tightening cycle is done and have priced in a rate cut later in the year. Still, the RBA hasn't ruled out rate hikes, with inflation still well above the 2% target.

The central bank needs to be sure that once inflation reaches the target, it can be sustained at that level and is likely to be very cautious before shifting policy and cutting rates. The RBA doesn't meet until May and barring a huge surprise will again keep rates unchanged.

Australia's Westpac consumer confidence declined 1.8% in March to 84.4, worse than the market estimate of -1.6%. The index has been below 100 since February 2022, indicative of prolonged pessimism about the economy. Consumer confidence took a hit after the 6.2% gain in February, as frustrated consumers didn't see any signs of a rate cut at the RBA's meeting earlier this month.

AUD/USD Technical

![]()

![]()

![]()

This is a follow-up analysis of our prior report, "CHF/JPY Technical: Potential major bullish trend exhaustion" dated 13 March 2024. Click here for a recap.

The CHF/JPY cross-pair has remained soft as it failed to surpass its 50-day moving average at around 170.00. The previous minor rally from the 11 Mar 2024 low of 167.08 was rejected at the 50-day moving average on 21 March 2024 and reversed sharply to the downside thereafter with a loss of -296 pips/-1.73% in the past three sessions as it printed an intraday low of 167.83 today, 26 March at this time of the writing.

Fig 1: 1-month rolling performances of G-10 CHF crosses as of 26 Mar 2024 (Source: TradingView, click to enlarge chart)

This recent bout of sharp downside reversal of the CHF/JPY has been attributed more to the CHF side of the equation as the Swiss National Bank (SNB) surprised market participants last Thursday, 21 March with a rate cut of 25 basis points (bps) to 1.5% on its key policy rate, its first cut in nine years, and ahead of the US Federal Reserve, Bank of England (BoE), and European Central Bank (ECB).

One of the push factors for enacting an earlier rate cut by SNB is the persistent strength of the franc that could erode the competitiveness of Swiss goods and services which in turn put a dent on economic growth prospects in Switzerland.

The CHF has weakened across the board against other major G-10 currencies and not surprisingly, the CHF is the weakest against the EUR with a loss of -2.5% based on a one-month rolling performance basis with the CHF/JPY coming in fifth position in the pecking order of CHF's weakness (see Fig 1).

Fig 2: CHF/JPY major & medium-term trends as of 26 Mar 2024 (Source: TradingView, click to enlarge chart)

Fig 3: CHF/JPY short-term trend as of 26 Mar 2024 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis, the major uptrend of CHF/JPY in place since the 13 January 2023 low of 137.44 has shown signs of bullish exhaustion. Firstly, it has traced out a bearish "Ascending Wedge" configuration from the 3 October 2023 low where such configuration/chart pattern typically appears at the end of a significant uptrend phase (see Fig 2).

Secondly, medium-term upside momentum has turned lacklustre as depicted by the observations seen in the daily RSI momentum indicator where it has flashed out a persistent bearish divergence condition since 10 January 2024.

Thirdly, the final straw came after the CHF/JPY broke below its 20-day moving on last Thursday, 21 March ex-post SNB.

In the short-term as depicted in its hourly chart, the latest price actions of the CHF/JPY have transformed into a minor downtrend phase after today's bearish breakdown below its minor ascending trendline from the 11 March 2024 minor low.

If the 169.00 key short-term pivotal resistance (also the 20-day moving average) is not surpassed to the upside, the CHF/JPY may continue to display further weakness to expose the 167.10 near-term support and its key support at 166.55 (the 200-day moving average & lower boundary of the "Ascending Wedge").

A daily close below 166.55 increases the odds of a major bearish breakdown scenario for the CHF/JPY that is likely to trigger the start of a potential major multi-month downtrend phase.

Conversely, a clearance above 169.00 negates the bearish tone for a choppy minor corrective rebound for the next intermediate resistances to come in at 170.00/20 and 170.70 (medium descending trendline from 22 February 2024 high).

![]()

![]()

![]()

OANDA Senior Market Analyst Kelvin Wong joins Jonny Hart to discuss this week’s key economic data and events. A relatively quieter week versus last week’s major central banks’ galore as we head into the Easter holiday with several key events and economic data to take note.

Firstly, risk of currency war is lingering around the horizon after China central bank, PBoC’s move to weaken the onshore Chinese yuan daily fixing on last Friday, 22 March that led the offshore yuan (CNH) to tumble by -0.8% against the US dollar to hit a two-week low. This move seems to be a deliberate attempt to maintain some form of exports’ competitiveness for China after the surprise rate cut from SNB ahead of the Fed, and ECB that has occurred on Thursday, 21 March that triggered a bout of US dollar strength resurgence. A further weakening of the yuan may spark the revival of currency war vibes as major exporters such as South Korea, and Singapore join in the bandwagon to weaken their domestic currencies against the US dollar which in turn increases the odds of a global risk off episode.

Lastly, we have the release of Australia’s monthly CPI data for February on Wednesday, 27 March, and the all important closely watch US PCE inflation data out on Friday, 29 March.

![]()

![]()

![]()

The Japanese yen is showing limited movement on Monday. In the North American session, USD/JPY is trading at 151.25, down 0.13%.

Yen can't find its footing

Last week's Bank of Japan was dramatic as the central bank raised interest rates for the first time since 2007. The move did not catch the markets completely by surprise, as some media reports ahead of the meeting said the BoJ would raise rates and investors were looking at both the March and April meetings as strong possibilities for a rate hike.

The yen did not respond to the rate hike with gains, as might have been expected. There are several reasons for this. First, the actual tightening was limited, with rates rising from -0.10% to 0.10%. This means that although the BoJ rate is now in positive territory, the move had little impact on the wide USD/JPY rate differential. BoJ Governor Ueda said after the meeting that despite the hike, monetary policy would remain accommodative, saying that there was "some distance to go" until inflation climbs to the 2% target.

As well, many investors approached the BoJ meeting with a "buy the rumour, sell the fact" approach and this resulted in heavy selling of the yen after the rate announcement. The yen slipped 1.60% last week and dropped as low as 151.86, its lowest level since November 2023.

The Japanese yen has dropped to levels that could invite intervention – the Ministry of Finance intervened last September and October when the yen dropped to around the 152 line. If the yen continues to lose ground, the threat of intervention will become greater.

In the US, the markets have priced in three rate cuts this year, and the Fed also projected three cuts this year at last week's meeting. However, Atlanta Federal Reserve President Raphael Bostic sounded hawkish on Friday when he said that he expects only one quarter-point cut this year.

Bostic said that he was "definitely less confident than I was in December" that inflation will continue to drop towards the 2% target, as he noted that inflation remains stubbornly high and the US economy has been more resilient than he expected.

USD/JPY Technical

![]()

![]()

![]()

The Australian dollar has started the week with slight gains, after sliding 0.86% on Friday. In the European session, AUD/USD is trading at 0.6530, up 0.24%.

PBoC move sends Aussie sharply lower

The Australian dollar ended the week with sharp losses after China's central bank set the daily fixing of the Chinese yuan lower than expected on Friday. The PBoC weakened the yuan in order to boost China's struggling economy and the move led to an AUD/USD sell-off on Friday. China is Australia's number one trading partner, and currency interventions such as the PBoC move can have a major impact on the Australian dollar.

It's a light day on the data calendar, which means we can expect a quiet day for AUD/USD. The only tier-1 event is US New Home Sales, which is expected to rise to 680,000 in February, up from 661,000 in January.

Australia releases Westpac Consumer Sentiment on Tuesday, with the markets braced for a decline of 1.6% for March. This follows a sparkling 6.2% gain in February, as consumer confidence climb sharply after the Reserve Bank of Australia held interest rates earlier in February. Consumers expressed optimism that the RBA had winded up its rate-tightening cycle.

In the US, the markets have high hopes for three rate cuts this year, and the Fed's "dot plot" projection at last week's meeting also projected three cuts this year. However, Atlanta Federal Reserve President Raphael Bostic dampened the mood on Friday when he said that he expects only one quarter-point cut this year. Bostic said that he was "definitely less confident than I was in December" that inflation will continue to drop towards the 2% target.

AUD/USD Technical

![]()

![]()

![]()

This is a follow-up analysis of our prior report, "Hang Seng Index Technical: The countertrend rebound phase may have ended" dated 5 March 2024. Click here for a recap.

In the past two weeks, China, and Hong Kong benchmark stock indices (CSI 300, Hang Seng Index, Hang Seng TECH Index & Hang Seng China Enterprises Index) have traded sideways after recording gains of between +16% to +24% from their respective early February lows to recent mid-March highs.

These recent bouts of positive performances have propelled China and Hong Kong to be the top-performing major stock markets in February and are supported by the absence of a strong US dollar environment that reduces the risk of capital outflows as China remains mired in a deflationary risk spiral as well as ongoing high tech trade war with the US since 2018.

Hence, the recent rallies and outperformance of the key China and Hong Kong benchmark stock indices have been indirectly supported by a stable Chinese yuan where the CNH (offshore yuan) has traded in a tight range of 0.7% against the US dollar between 5 February to 12 March.

Last Thursday, 21 March, the Swiss National Bank (SNB) engineered a surprise on market participants by enacting a rate cut of 25 basis points (bps) to 1.5% on its key policy rate, its first cut in nine years, and ahead of the US Federal Reserve, Bank of England (BoE), and European Central Bank (ECB).

One of the push factors for enacting an earlier rate cut by SNB other than a clear deceleration in inflationary trend (annualized core inflation rate has remained below 2% since May 2023) is the persistent strength of the franc that could erode the competitiveness of Swiss goods and services which in turn put a dent on economic growth in Switzerland.

The EUR/CHF cross pair has accelerated its decline in the past three years where it tumbled by -17% to print a close of 0.9270 on 5 January 2024, a fresh all-time low on a closing level basis since the surprise EUR/CHF unpeg on 15 January 2015 (intraday low of 0.8600 with a daily close of 0.9753).

The CHF tumbled after the surprise SNB's decision; it fell by -1% against the EUR to its weakest level since July 2023. Also, it dropped -1.2% against the US dollar to hit a fresh four-month low.

Interestingly, the offshore yuan (CNH) tumbled by -0.8% against the US dollar to print a two-month low last Friday, 22 March after the China central bank, PBoC set a weaker-than-expected daily fixing on the onshore yuan (CNY).

This latest set of FX policy moves by PBoC is likely to have signaled a willingness to sacrifice some form of capital outflows over maintaining exports' competitiveness to drive economic growth, and to fill the gap in the absence of robust domestic demand.

If the US dollar continues to strengthen due to the Fed's less dovish stance (in no hurry to cut rates), it may lead to a bout of engineered currency devaluations among major exporters such as South Korea and Singapore which is likely to put pressure on PBoC to weaken the CNH further to make up for a further potential loss of trade competitiveness.

Overall, a persistent US dollar strength trend may trigger "beggar-thy-neighbour" currency war-liked monetary policies among exporters.

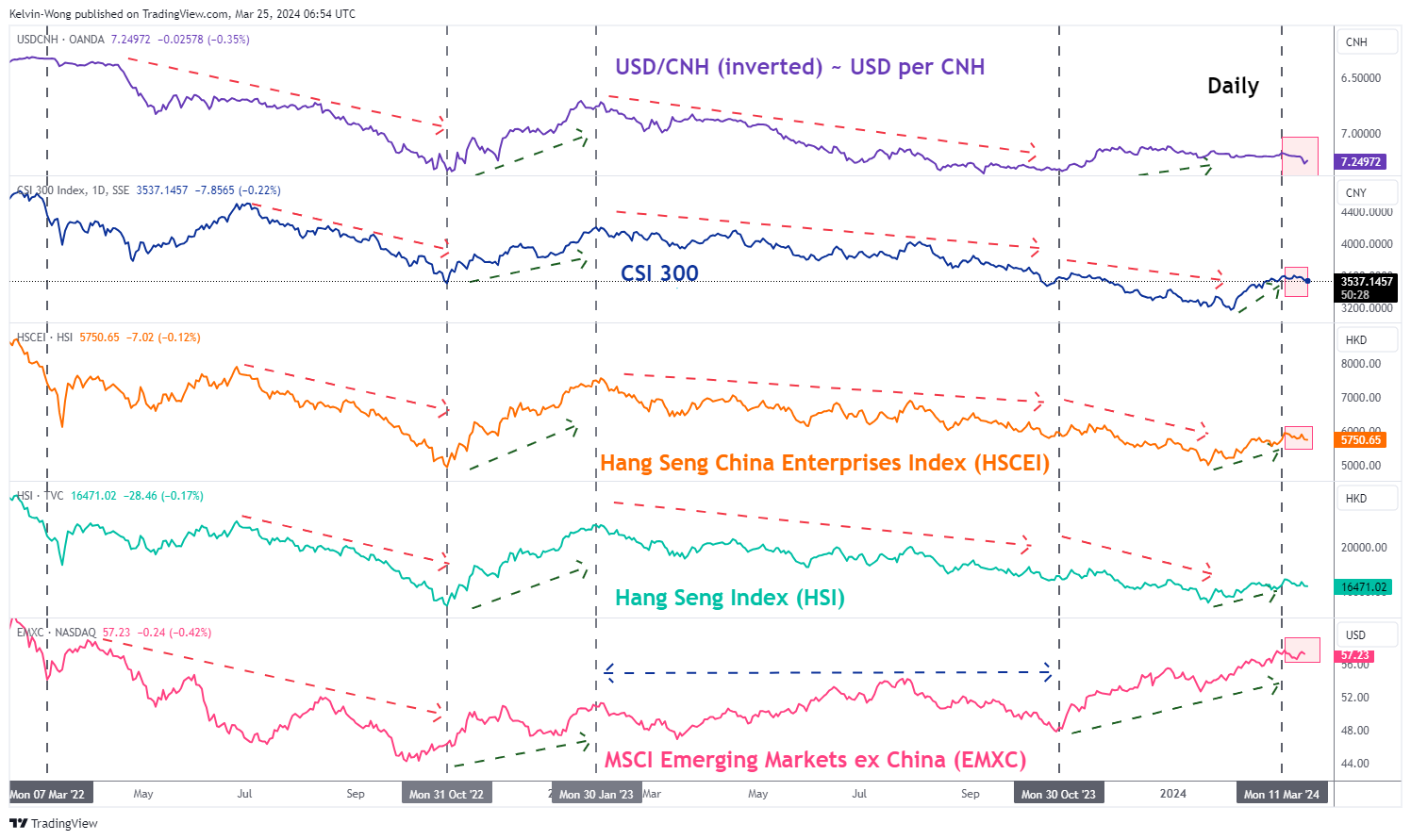

Fig 1: CNH/USD direct correlation with CSI 300, HSCEI & HSI as of 25 Mar 2024 (Source: TradingView, click to enlarge chart)

In the past two years, periods of significant weakness in the CNH (offshore yuan) against the US dollar have triggered a negative feedback loop back into the China and Hong Kong stock markets but to a lesser extent in emerging stock markets excluding China (see Fig 1).

Therefore, the recent softness seen in the CNH may trigger another round of potential multi-week bearish movements in the CSI 300, Hang Seng China Enterprises Index, and Hang Seng Index.

Fig 2: Hong Kong 33 Index major trend as of 25 Mar 2024 (Source: TradingView, click to enlarge chart)

Fig 3: Hong Kong 33 Index short-term trend as of 25 Mar 2024 (Source: TradingView, click to enlarge chart)

The price actions of the Hong Kong 33 Index (a proxy on the Hang Seng Index futures) have staged a bearish breakdown below its former ascending channel support in place since the 22 January 2024 low and its 20-day moving average on last Friday, 22 March.

In addition, the daily RSI momentum has also broken below its key parallel ascending support and just breached below the 50 level which indicates a potential revival of medium-term bearish momentum.

In the lens of technical analysis, this latest set of bearish elements suggests the recent rally of +16% from the 22 January 2024 low of 14,777 has taken the form of a "bearish flag" configuration, aka countertrend rebound motion within its major and long-term secular bearish trend phases (see Fig 2).

Last Friday's bearish breakdown seen in the "bearish flag" and its daily RSI suggested a likelihood that the bearish impulsive down move sequence has resumed.

If the 16,960 key short-term pivotal resistance is not surpassed to the upside, the Index may see a further potential decline to expose the next intermediate supports at 16,135 (also the 50-day moving average), and 15,730 (see Fig 3).

However, a clearance above 16,960 negates the bearish tone to see a retest on the 17,230 minor swing high area of 13 March 2024, and above it sees the medium-term pivotal resistance coming in at 17,570/600.